4 steps to complete your EU Taxonomy reporting

28.06.2024

·

Martina Bortot

The EU Taxonomy is a comprehensive classification system developed by the European Union with the aim of identifying economic activities that can be considered environmentally sustainable. Companies that fall under the scope of the Corporate Sustainability Reporting Directive (CSRD) will be asked to conduct EU Taxonomy reporting, following the requirements set out by the Taxonomy Regulation. To comply, non-financial companies must perform a EU Taxonomy assessment to determine the sustainability of each of their activities and report three relevant financial KPIs: Turnover, Capital Expenditure (CapEx), and Operating Expenditure (OpEx).

This article aims to provide an easy 4-step process to assist non-financial companies in conducting their EU Taxonomy assessment.

1. Identify your economic activities

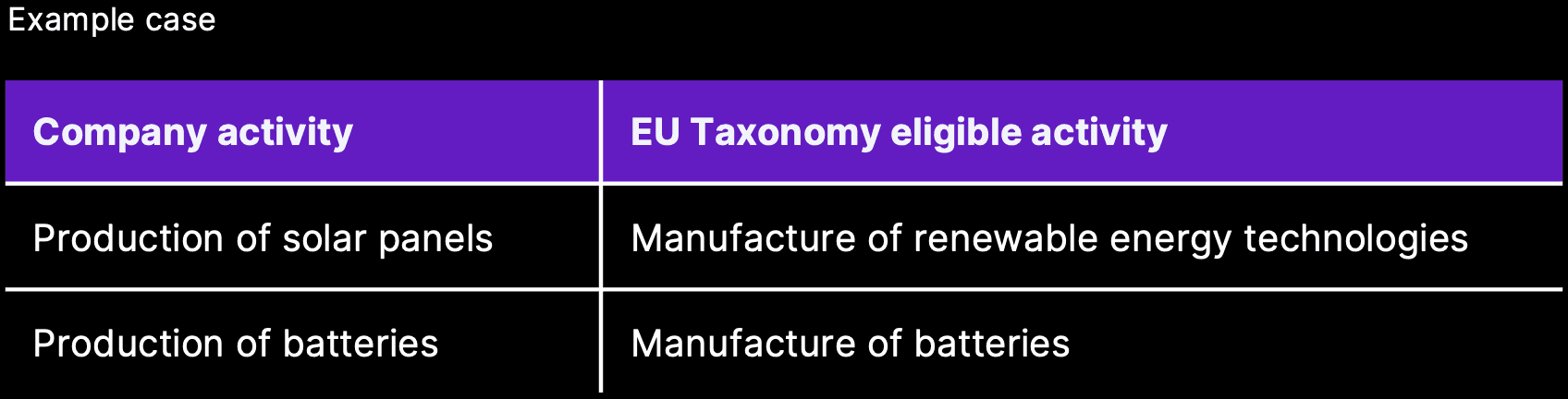

The initial step of your Taxonomy assessment involves creating a comprehensive overview of your company's economic activities. Begin by identifying and outlining the primary sources of your business operations, providing each activity with a clear title and description. For instance, a manufacturing company specializing in energy technologies might list activities such as "Manufacturing of solar panels" and/or "Production of batteries."

2. Calculate Taxonomy-eligibility

Once the mapping process is complete, the next step involves verifying which of these activities are covered by the EU Taxonomy by reviewing the list of "Taxonomy-eligible" activities (available in the EU Taxonomy Compass). The EU Taxonomy has established a defined set of eligible economic activities, which is in continuous development and will be expanded over time.

In the earlier example, the manufacturing company could identify two eligible activities under the EU Taxonomy for both "Manufacturing of solar panels" and "Production of batteries."

To determine eligibility, companies can use the NACE industry classification system as a reference, since each EU Taxonomy activity specifies applicable NACE codes.

Next, it’s important to confirm which environmental objectives each activity contributes to. The EU Taxonomy sets out six environmental objectives that economic activities can substantially contribute to:

Climate Change Mitigation

Climate Change Adaptation

Sustainable Use and Protection of Water and Marine Resources

Transition to a Circular Economy

Pollution Prevention and Control

Protection and Restoration of Biodiversity and Ecosystems

Each activity should contribute to at least one environmental objective, although many activities may contribute to multiple objectives. It is important to verify this early on, as these environmental objectives will be relevant in Step 3.

Lastly, calculate the proportion of Taxonomy-eligible activities for the three financial KPIs (Turnover, CapEx, and OpEx). For instance, in the case of Turnover, calculate the share of Turnover derived from taxonomy-eligible activities relative to the total Turnover of the company.

3. Calculate Taxonomy-alignment

The assessment continues with the calculation of Taxonomy-alignment activities. To be classified as “environmentally sustainable” under the Taxonomy, an economic activity must satisfy 3 overarching conditions (refer to the EU Taxonomy Compass for all applicable criteria for eligible activities).

Substantial Contribution Criteria: The company has to evaluate whether the activity under analysis satisfies the list of requirements for the corresponding Taxonomy activity.

Do No Significant Harm (DNSH) Criteria: The company has to assess whether the activity under analysis does not harm any of the other five environmental objectives by complying with the specific “no harm” criteria established for each.

Minimum Social Safeguards: the company has to comply with the international standards and guidelines on human rights and labor practices. This condition requires a one-time company-level assessment, rather than an activity-level assessment, and does not need to be repeated for each activity.

Activities will be considered Taxonomy-aligned only if all the three conditions outlined above are met. After completing the alignment assessment, you should proceed to calculate the proportion of Taxonomy-aligned activities for the three financial KPIs (Turnover, CapEx, and OpEx). For instance, in the case of Turnover, calculate the share of Turnover derived from only the taxonomy-aligned activities relative to the total Turnover of the company.

4. Report EU Taxonomy results

Finally, the last step is to finalize the assessment by reporting the results of the Taxonomy-eligibility and Taxonomy-aligned KPIs. For non-financial companies, the EU Taxonomy reporting disclosures have to be structured using the templates presented in Annex II of the Disclosures Delegated Act (see snapshot below).

Source: Disclosure Delegated Act, ANNEX II - TEMPLATES FOR THE KPIs OF NON-FINANCIAL UNDERTAKINGS

Final remarks

The EU Taxonomy reporting presents a significant challenge for most companies. Its complex framework and extensive assessment requirements can be difficult to manage. A major difficulty lies in the room for interpretation. Often, it is unclear how to accurately identify economic activities or how to interpret the criteria for substantial contribution and DNSH.

We recommend not underestimating the reporting effort, especially within the context of the CSRD reporting requirements. Start early to plan the timeline and resources needed within the company to conduct the Taxonomy assessment. From our experience, the first time of reporting is typically the most challenging. Therefore, companies that start early are better positioned to establish a solid foundation, ensuring that future reporting cycles are easier and more efficient.

If you need help with your EU Taxonomy assessment, contact us to learn more about how Atlas Metrics can help you simplify ESG compliance.